Our Events

Supply strategy: how to enter EV supply markets in Southeast Asia

13 December 2023Chinese EV automakers have recently been heavily pushing into the markets in Southeast Asia. And...

EV Charging Market: it’s not only about chargers

10 November 2023Electric mobility is often discussed around the most important hardware – the car. But there...

Fleet Management: why companies electrify their fleets

04 October 2023In a seeming mindset tipping point on the future of electrification, electric vehicle (EV) sales...

The best books on how to make transport & mobility sustainable

03 October 2023If you are interested in the future of mobility, you are constantly in search of...

Extreme weather events: 3 basic facts about climate change

22 September 2023“The recent flood in Ahrtal (Germany) is a sign of the man-made climate change.” Or...

Klimawandel durch CO2 – Verkehr am Pranger

03 November 2020Der Klimawandel ist in aller Munde, speziell der Verkehrssektor...

How mobility & transportation can decarbonize without just taking symbolic action

29 June 2020It’s an old discussion with a lot of biased arguments being repeated continuously. What is...

The Best Podcasts from Mobility, Transportation & Automotive

14 May 2020If you are interested in new mobility topics, you might know that there are plenty...

Covid-19: Do we need to restrict our mobility?

05 May 2020The Covid-19 pandemic has sent many countries into a state of shutdown where major parts...

Mobility and Travel in Post-Corona

15 April 2020The Corona pandemic has caused huge disruptions in travel and mobility.

The Mobility of the Future – Showcase Singapore

30 March 2020When it comes to examples for how the mobility of the future might look like,

My Favorite Mobility Blogs

26 March 2020If you are interested in the future of mobility, you are constantly in search of...

Mobilitätsmarkt – die Musik spielt nicht bei uns

25 November 2019Wenn wir in Deutschland über die Mobilität der Zukunft diskutieren,

Klimaschutzpaket – wer hat sich das ausgedacht?

24 September 2019Seit der Vorlage des Klimaschutzpaketes durch die Bundesregierung...

Deutsche Batteriezellproduktion – das nächste Milliardengrab?

24 May 2019Volkswagen hat den Strategieschwenk auf Elektromobilität vollzogen...

The automotive disruption and its impact on OEMs and suppliers

09 May 2019Do you remember the last time you took a picture with an analogue,

Supply strategy: how to enter EV supply markets in Southeast Asia

13 December 2023Chinese EV automakers have recently been heavily pushing into the markets in Southeast Asia. And not only do they push on the sales side to use ASEAN markets to sell their latest EV models. They have also started establishing production sites for electric vehicles or EV batteries. Especially Thailand has been a major hub for investment in EV manufacturing recently.

Thailand as emerging hub for EV production

Thailand is a premier trade ally of China and has been promoting the adoption of electric cars by offering a subsidy for each EV of up to 150,000 Baht along with other incentives such as import tax cuts. It is positioning itself as a regional hub for EV production and has attracted investment from several major Chinese automakers.

Chinese car manufacturer SAIC Motor has just opened its first battery plant for electric vehicles in Chonburi province. Neta Auto has also started production at its first overseas electric vehicle plant in Thailand with an annual capacity of 20,000 EVs. BYD has signed a deal to build its first overseas plant in Thailand, which is about to start operating in 2024 with a planned annual capacity of 150,000 cars to supply Southeast Asian markets. Changan Automobile just signed an agreement with Thailand’s Board of Investment (BoI) to build an electric vehicle factory in the coastal Rayong province. Other carmakers (e.g. from Korea or Japan) are planning to follow suit.

OEMs entering ASEAN have to ensure supply for the new plants

Car OEMs enter emerging markets such as ASEAN since they are expecting strong market growth. A local production is usually favorable for several reasons. It reduces transportation cost to meet the local demand. It avoids instable customs situations (depending on FTAs) with relatively high taxes on imported finished goods. And it reduces cost uncertainty due to hardly predictable currency fluctuations. Establishing a reliable and qualified supply base is key for thriving in these markets.

When assessing the local supplier landscape, carmakers usually find several constraints. Local suppliers oftentimes have quality and tolerances below usual standards. Their incumbent suppliers usually have limited local presence and face high investment needs and risks when moving to new markets. Specific local business mindsets with lack of transparency can be a serious challenge. To achieve appropriate local supply, carmakers need to find the right approach for the local supply market in order to meet tight SOP timelines.

SEA Supply Base constraints require specific supply approach

Car OEMs have several options to mitigate these supply base risks. They can increase in-house production with higher vertical integration for strategic components such as the battery. They can develop local suppliers to achieve required performance levels. They can leverage developed suppliers from other industries. They can localize strategic incumbent suppliers and support them in ramping up a local supplier park. Or they can finally exploit existing production lines, tools and infrastructure of incumbent suppliers (in low cost countries) and import components.

These options need to be assessed and evaluated for Thailand or other ASEAN markets. In any case it can be expected that on its way to become sustainable and reduce carbon dioxide emissions, Southeast Asia will have a thriving EV production and supplier landscape in the upcoming years.

EV Charging Market: it’s not only about chargers

10 November 2023Electric mobility is often discussed around the most important hardware – the car. But there is another important hardware besides the electric vehicle – the charger. And when talking about EV charging, there is more than the hardware – it’s software and services.

EV Charging market to grow rapidly until 2030

Analysing the EV charging market for several years and forecasting the market development reveals an attractive, dynamic market for EV charging hardware, software and service providers. The overall market is expected to grow rapidly until 2030 and beyond. Here are some key insights when looking at EV charging markets by region, use case, component, charger and vehicle type.

China has the lead, North America is lagging

Overall market growth is mainly driven by China with its large EV fleet. When comparing North America and Europe, North American EV fleet penetration is expected to lag Europe’s development. The other Asian markets besides China are still small but with some dynamic growth perspectives from a small overall EV fleet. It is expected that the market will mature in most regions after 2030. This will go along with lower growth rates.

Market size and growth differ heavily dependent on the use cases (depot, residential, public etc.). with the increasing EV penetration of personal vehicles, residential charging will probably become the most important use case. But depot charging is expected to be a major use case as well due to the ongoing electrification of last-mile delivery fleets and city / school buses. En-route fast charging will grow slower since network expansion will be limited as soon as more emphasis is put on charger utilization. Workplace and public charging will be interesting niche markets compared to the size of the use cases previously discussed.

Hardware will be the dominant EV charging components but services & software grow faster. But with average prices for chargers expected to decline, EV charging software and services (e.g. fleet management, maintenance) will be the components growing faster than the chargers themselves. Especially charger maintenance services can be an attractive market in the future.

HPC heavily used in en-route charging

Although AC chargers are large in terms of sales volume, DC chargers represent the larger market when it comes to charger types. The average prices for a DC charger is significantly higher than the average price of an AC charger. Within the DC charger segment, high-power chargers (HPC) will grow since they will be frequently used in en-route fast charging. Ultra high power charging (UHPC) above 350 kW will be a niche with low volumes. It is mostly used in en-route fast charging for trucks. For these use cases other technologies such as fuel cell might come into play.

The vehicle per charger ratio will increase with growing EV fleets for most types of vehicles (light, truck, bus etc.). The ratio varies across use cases. For example, en-route fast charging will be mostly used for trips exceeding the battery range. The number of vehicles using these chargers will be higher than for residential or depot charging. Therefore, the vehicles per charger ratio is relatively high.

The EV charging market is complex and moving quickly. Detailing these overall market trends will provide further insights for EV charging players and investors.

Fleet Management: why companies electrify their fleets

04 October 2023In a seeming mindset tipping point on the future of electrification, electric vehicle (EV) sales have soared globally. From 2019 to 2021 the sales numbers quadrupled. Worldwide, a 75% increase in 2022 over 2021 shows EV transition is going strong which goes along with a need for electric vehicle fleet management.

Benefits of electric vehicles

In the long run, electric vehicles will have a lower total cost of ownership (TCO). But the initial purchase costs still outweigh the attraction for buyers compared to cheaper internal combustion engine cars (ICEs). While the EV purchase price can be significantly higher, the actual individual cost comparisons (aside from batteries) are rather surprising.

What makes EVs more expensive?

- Batteries are the main driver for higher costs in EVs.

- EV depreciation & interest rates are higher than ICEs due to a higher purchase price.

- Tires must be replaced more often with EVs due to more weight and torque which accelerates wear & tear.

What are the TCO advantages of EVs?

- EV maintenance is less frequent and cheaper as there are fewer moving parts.

- Electrical power is cheaper (upt to 50%) than gasoline.

- Taxes for EVs can be lower than ICEs due to government incentives.

- Many countries offer subsidies for EV purchases.

So, in the long run scenario, an electric vehicle that has a longer lease-life and racks up a lot of mileage continues to make TCO more attractive than an ICE vehicle.

And this is especially important for commercial fleets.

Electrification Planning

Companies running transport fleets (e.g. last-mile delivery) need to maintain uninterrupted business operations and utilize their vehicle assets to the maximum. They also want to make any structural changes as cost effective as possible. Simply purchasing electric vehicles & chargers and putting them on routes without a strategy will disrupt all of the above.

Fleet electrification should happen in increments. That means any fleet will be running mixed EV & ICE fleets for a while. During that time, a company learns how to run & charge EVs without hurting operations. It also allows for planned purchasing in line with current vehicle-life durations or leasing contracts.

To know which vehicles to electrify when, analysis of current fleet vehicles, routes, ranges, standing times and electrical infrastructure is paramount.

Most transport fleets are depot-based. So which depot will it be? What is its electrical grid capacity and energy output? Is the company running last-mile or mid-mile delivery? If so, what kind of ranges are they covering, in how many shifts? Is operational vehicle & routing data available, like telematics? If not, do they have historical data?

And again, how much and how cost-effective is the total cost of ownership (TCO)?

No wonder that many fleet managers are unwilling to take on such complexity.

Vehicle & Infrastructure Selection

There is no doubt that most companies are entering completely new territory when they plan their e-fleet transition. Many start by formulating an electric vehicle policy to set out the general goals and framework for such a change. Doing so helps clarify which EV models can be chosen, charging costs and locations, or what happens if an employee resigns. Within such a framework, requirements planning can begin, balancing tasks and solutions.

The key questions to be answered here

- What are the tasks of the e-fleet?

- Which ranges are necessary?

- Which delivery times should be realized?

These requirements are compared to the existing options:

- Configuration options of EVs available on the market.

- Total Cost of Ownership (TCO) estimates, including tax aspects and subsidies.

Involving internal and external stakeholders — like logistics, facility management, purchasing, drivers, etc. — at an early stage, is sound advice.

Setting up the corresponding charging infrastructure is equally essential. Five key areas are important here:

- How many charging points does the company need and what performance do they have to offer?

- What should load management look like?

- What are the costs for installing and operating these charging points?

- Should there be charging points for employees at home (charging@home)?

- How is charging outside the company billed?

Again, early-stage stakeholder involvement (like electricity providers, hardware vendors, installation experts) is advisable.

Pillars of Fleet Transition

Whatever the case, the nature and complexity of these tasks makes careful planning of fleet transition and electric vehicle fleet management more than advisable. The proverbial “jump into the deep end” is a risk better not taken. Therefore, the pillars of fleet transition are fleet analysis, infrastructure analysis & guidance.

The fleet analysis considers a fleet’s electrification potential based on historical data and telematics data. With a software, users collect relevant data on the current vehicles and create an analysis of the electrification potential of a fleet. Based on this analysis, fleet operators can identify carbon dioxide (CO2) reduction potential and receive recommendations for suitable EV replacements that best meet their specific requirements.

The infrastructure analysis is the basis for an optimal e-fleet charging infrastructure. It considers the necessary number of charging stations and their optimal locations, suitable manufacturers and models and finally the charging and load management — including a feasibility check with an electrician. It also takes the integration of charging options for employees at home and public charging options into account. The specific charging management is then carried out with a dedicated Charge Management software. It should be optimized for business continuity and costs, and charging schedules need to be integrated into day-to-day operations.

The third conceptual pillar is guidance on the electrification journey. This allows for specific tailor-made solutions for a fleet’s individual needs and requirements. It also includes basic e-mobility training to make relevant knowledge available to all internal stakeholders. Other topics include educating on subsidies and tax breaks.

Conclusion

Overall, a strategic electrification plan is a smart, sustainable and worthwhile (but not trivial) undertaking. Early planning, the availability of all relevant information and a realistic view of budgeting and costs are crucial. In the long-run, a fully-fledged electric vehicle fleet management should be in place.

The best books on how to make transport & mobility sustainable

03 October 2023If you are interested in the future of mobility, you are constantly in search of good books dealing with the topic. I recently curated a list of books that I think are a must-read when it omes to sustainable mobility. You can find my list of the best books on how to make transport & mobility sustainable at Shepherd.

At the top my list “The future is Asian” by Parag Khanna. The book shows how the future of our planet will be decided in Asia. It teaches us that when we aim to tackle climate change with impactful measures, it is not about America or Europe but about Asia.

With its tremendous size and growth in population, Asia will be the dominant continent in the world and therefore be key to solving the climate crisis.

Shepherd is a great resource to find the best books in almost any category you can think of. I also shared the list of my best reads in 2023 with Shepherd, you can find it here.

Extreme weather events: 3 basic facts about climate change

22 September 2023“The recent flood in Ahrtal (Germany) is a sign of the man-made climate change.” Or more general: “The extreme weather event X in country/ region/ city Y has been caused by man-made carbon dioxide emissions.”

These statements or similar versions have recently been all over the media. And as with many things that are being repeated frequently, they are simply not true. The distorted truths communicated on many news outlets have been outlined by German climate scientist Hans von Storch in his latest book on the historical evolvement of climate sciences.

His major insights sound basic but are oftentimes forgotten in the public discussion.

Climate change has two components

Climate change has two components

The first one is a natural, stochastic one. It’s like noise. Temperature averages are fluctuating over time and they will continue to do so. This has nothing to do with external forces. The second one is an external, man-made component. This one is due to increased levels of carbon dioxide emitted by man. This is the climate change that is often referred to on the media.

These components are hard or nearly impossible to distinguish. In case of extreme events (e.g. floods, fires etc.) both components come into play. Claiming a single weather event is due to one of those components only is just not based on the scientific facts.

Climate change is currently being discussed from two angles

One is the change of geo-physical climate system. Here we are talking about climate in the sense of weather statistics. This is very well covered by climate sciences.

The second one is the discussion of expected consequences such as tipping pints and extreme weather events. This discussion is very much a political one.

Climate change needs to be tackled in two complementary ways

When it comes to actions on responding to the climate change described above, two approaches need to be balanced.

In the mitigation approach, we need to reduce carbon dioxide emissions to lower carbon dioxide levels and limit man-made climate change. This usually occurs on a national/supra-national level. At the same time we need the adaptation approach. Our societies need to adapt to climate change that will occur despite mitigation since reduction of carbon dioxide emissions will not prevent future extreme events such as floods etc. This is a task on regional and local level.

If we are aware of these basic climate change facts, it is possible to separate climate sciences from politics. And the task for politics is then to balance mitigation and adaptation strategies in a reasonable ratio.

Now, near, next: Transforming manufacturing disruption into opportunities

In today’s volatile and complex world, unexpected risks are abundant, and manufacturers face countless technological, social, environmental, economic, and market-related challenges. Disruption in manufacturing can present unexpected risks, but it can also provide strategic opportunities for companies to innovate and evolve.

New customers, markets, materials, and technologies offer limitless possibilities for growth and expansion. Thus, manufacturers must transform their businesses continually, or they risk perishing. As business leaders, it is essential to recognise the potential of disruption and manage the unexpected risks to seize the strategic opportunities that come with it.

- What are the key disruptions that manufacturers face today, and how can they turn these challenges into opportunities for growth and innovation?

- How can manufacturers embrace new technologies, such as automation, AI, and IoT, to transform their operations and stay competitive in a rapidly evolving market?

- What role do sustainability and environmental concerns play in manufacturing, and how can companies leverage these trends to create more sustainable and profitable business models?

Now, near, next: Transforming manufacturing disruption into opportunities

In today’s volatile and complex world, unexpected risks are abundant, and manufacturers face countless technological, social, environmental, economic, and market-related challenges. Disruption in manufacturing can present unexpected risks, but it can also provide strategic opportunities for companies to innovate and evolve.

New customers, markets, materials, and technologies offer limitless possibilities for growth and expansion. Thus, manufacturers must transform their businesses continually, or they risk perishing. As business leaders, it is essential to recognise the potential of disruption and manage the unexpected risks to seize the strategic opportunities that come with it.

- What are the key disruptions that manufacturers face today, and how can they turn these challenges into opportunities for growth and innovation?

- How can manufacturers embrace new technologies, such as automation, AI, and IoT, to transform their operations and stay competitive in a rapidly evolving market?

- What role do sustainability and environmental concerns play in manufacturing, and how can companies leverage these trends to create more sustainable and profitable business models?

Now, near, next: Transforming manufacturing disruption into opportunities

In today’s volatile and complex world, unexpected risks are abundant, and manufacturers face countless technological, social, environmental, economic, and market-related challenges. Disruption in manufacturing can present unexpected risks, but it can also provide strategic opportunities for companies to innovate and evolve.

New customers, markets, materials, and technologies offer limitless possibilities for growth and expansion. Thus, manufacturers must transform their businesses continually, or they risk perishing. As business leaders, it is essential to recognise the potential of disruption and manage the unexpected risks to seize the strategic opportunities that come with it.

- What are the key disruptions that manufacturers face today, and how can they turn these challenges into opportunities for growth and innovation?

- How can manufacturers embrace new technologies, such as automation, AI, and IoT, to transform their operations and stay competitive in a rapidly evolving market?

- What role do sustainability and environmental concerns play in manufacturing, and how can companies leverage these trends to create more sustainable and profitable business models?

Now, near, next: Transforming manufacturing disruption into opportunities

In today’s volatile and complex world, unexpected risks are abundant, and manufacturers face countless technological, social, environmental, economic, and market-related challenges. Disruption in manufacturing can present unexpected risks, but it can also provide strategic opportunities for companies to innovate and evolve.

New customers, markets, materials, and technologies offer limitless possibilities for growth and expansion. Thus, manufacturers must transform their businesses continually, or they risk perishing. As business leaders, it is essential to recognise the potential of disruption and manage the unexpected risks to seize the strategic opportunities that come with it.

- What are the key disruptions that manufacturers face today, and how can they turn these challenges into opportunities for growth and innovation?

- How can manufacturers embrace new technologies, such as automation, AI, and IoT, to transform their operations and stay competitive in a rapidly evolving market?

- What role do sustainability and environmental concerns play in manufacturing, and how can companies leverage these trends to create more sustainable and profitable business models?

Now, near, next: Transforming manufacturing disruption into opportunities

In today’s volatile and complex world, unexpected risks are abundant, and manufacturers face countless technological, social, environmental, economic, and market-related challenges. Disruption in manufacturing can present unexpected risks, but it can also provide strategic opportunities for companies to innovate and evolve.

New customers, markets, materials, and technologies offer limitless possibilities for growth and expansion. Thus, manufacturers must transform their businesses continually, or they risk perishing. As business leaders, it is essential to recognise the potential of disruption and manage the unexpected risks to seize the strategic opportunities that come with it.

- What are the key disruptions that manufacturers face today, and how can they turn these challenges into opportunities for growth and innovation?

- How can manufacturers embrace new technologies, such as automation, AI, and IoT, to transform their operations and stay competitive in a rapidly evolving market?

- What role do sustainability and environmental concerns play in manufacturing, and how can companies leverage these trends to create more sustainable and profitable business models?

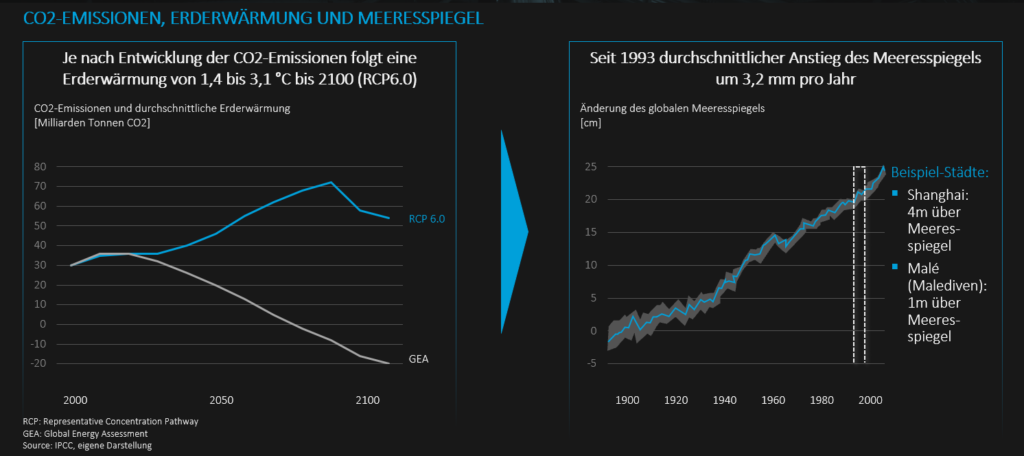

Klimawandel durch CO2 – Verkehr am Pranger

03 November 2020Der Klimawandel ist in aller Munde, speziell der Verkehrssektor wird scharf attackiert für seine hohen CO2-Emissionen. Wie ist die Faktenlage und welche Verantwortung ergibt sich daraus für unsere Mobilität der Zukunft?

Die weltweiten CO2-Emissionen sind massiv angestiegen,

ein dramatischer Anstieg des Meeresspiegels wird erwartet

Die weltweiten CO2-Emissionen sind stark gestiegen und nehmen weiter zu. Für die Zukunft lässt sich daraus eine globale Erderwärmung von (abhängig vom Szenario) 2 bis 6 Grad prognostizieren. Dies wird einen signifikanten Anstieg des Meeresspiegels zur Folge haben, der viele Gegenden und einige prominente Städte unmittelbar gefährdet. Die chinesische Stadt Shanghai liegt 4 Meter über Meeresspiegel, Malé auf den Malediven sogar nur einen Meter. Die Auswirkungen für die genannten Städte wären dramatisch.

CO2-Emissionen, Erderwärmung und Meeresspiegel

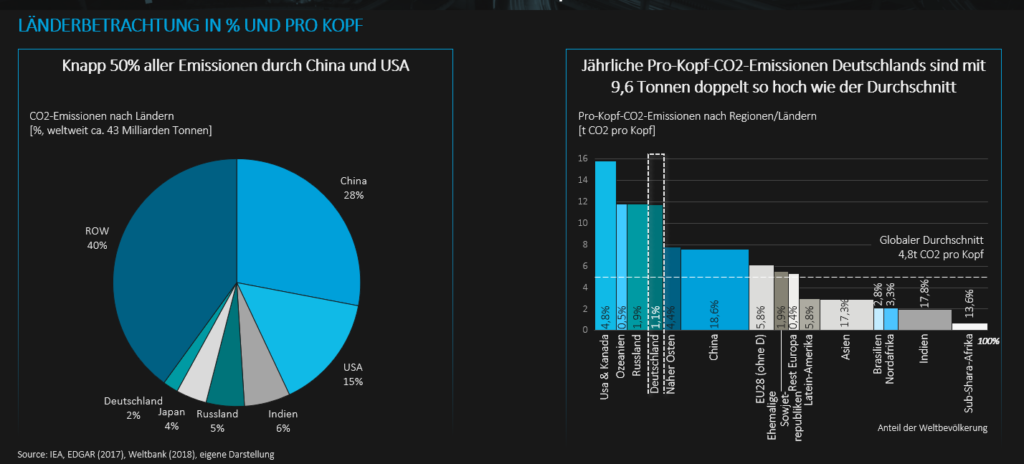

Knapp 50% der CO2-Emissionen werden durch China & USA verursacht,

westliche Industrienationen mit höchstem Pro-Kopf-Ausstoß

Schaut man sich an, wo die CO2-Emissionen herkommen, so muss man feststellen, dass fast die Hälfte der CO2-Emissionen von China, den USA und Indien verursacht werden. Deutschland emittiert ungefähr 2%. Eine globale Lösung des CO2-Problems wird also nur gemeinsam mit den Top-Emittenten möglich sein. Bei den Pro-Kopf-Emissionen liegen klassische westliche Industrienationen wie USA, Kanada und Australien an der Spitze, wenn man einmal von einigen verhältnismäßig kleinen Öl-Staaten im Nahen Osten absieht. Deutschland liegt mit ca. 9 Tonnen pro Kopf ungefähr doppelt so hoch wie der globale Durchschnitt.

Länderbetrachtung in % und pro Kopf

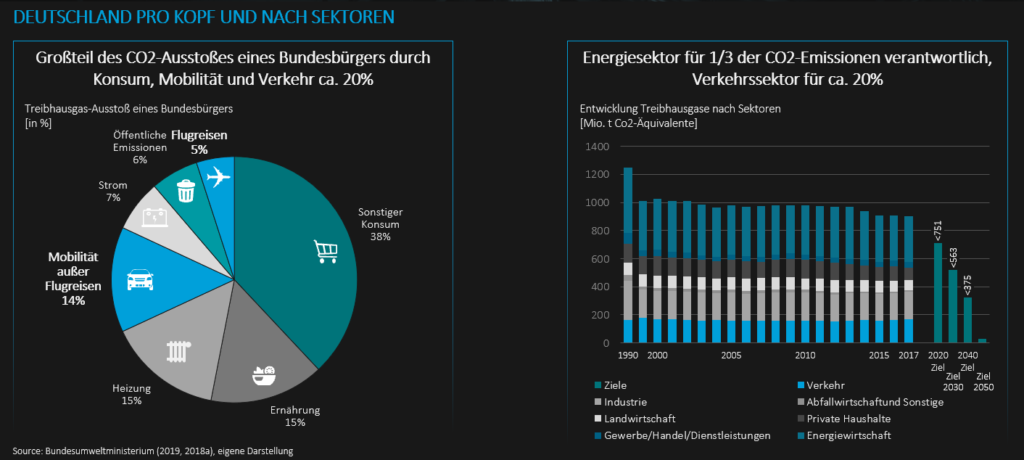

Der Großteil aller deutschen CO2-Emissionen entsteht durch Konsum,

Mobilität & Verkehr machen knapp 20% aus

In Deutschland werden ungefähr 20% der CO2-Emissionen durch den Verkehr erzeugt. Dies lässt sich sowohl in der Betrachtung eines Durchschnittsbürgers als auch in der Verteilung nach Sektoren erkennen. Während die Emissionen in den Bereichen Energiewirtschaft und Industrie seit 1990 zurückgegangen sind, müssen im Verkehrssektor steigende Emissionen konstatiert werden. Der Löwenanteil des CO2 kommt dabei aus dem Straßenverkehr, wo eine steigende Zahl an Fahrzeugen und größere Motoren die Effizienzverbesserungen beim Verbrennungsmotor überkompensiert hat. Was ist also zu tun?

Deutschland pro Kopf und nach Sektoren

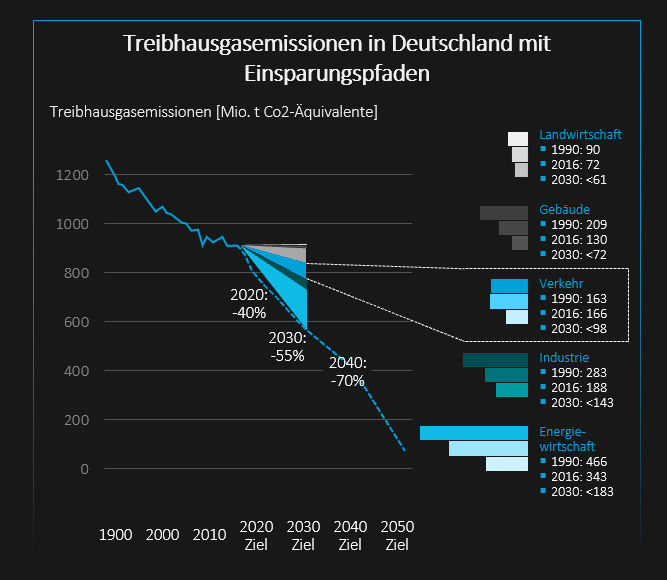

Klimaschutzplan der Bundesregierung mit ambitioniertem Einsparziel für den Verkehrssektor

Die Antwort der Bundesregierung sieht im Klimaschutzplan einen Dekarbonisierungspfad für alle Sektoren vor. Für den Verkehrssektor ergibt sich eine angepeilte Emissionsreduktion bis 2030 um ca. 40% bezogen auf das Referenzjahr 1990. Wie kann diese Herkulesaufgabe gelingen?

Einsparungspfade in Deutschland

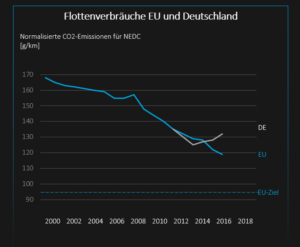

Zur Verfolgung der Dekarboniserungsziele muss Deutschland im Straßenverkehr die ambitionierten CO2-Flottenziele der EU erreichen

Im Straßenverkehr gibt es bereits seit langer Zeit verbindliche Vorgaben der EU. Zur Verfolgung der Dekarbonisierungsziele und Vermeidung von Strafen muss Deutschland die ambitionierten CO2-Flottenziele der EU erreichen. Das EU- CO2-Flottenemissionsziel liegt bei 95 g/km ab 2021. Aufgrund einer hoch motorisierten Fahrzeugflotte (z.B. mehr SUVs) steigt der durchschnittliche CO2-Ausstoß in Deutschland seit 2015. Für Neu-PKW lag er 2018 bei 130g/km. Ab 2021 sind Strafzahlungen bei Nichterreichung der Ziele von 95 Euro pro g CO2/km für jeden verkauften Neu-PKW fällig. Zur Vermeidung von Strafzahlungen ist deshalb bis 2021 ist eine Reduktion des Flottenverbrauchs um 30% nötig.

Flottenverbräuche EU und Deutschland

Der zukünftige Straßenverkehr muss einen Mix aus optimierten Verbrennern, Hybriden und Elektrofahrzeugen beinhalten

Die angestrebten Ziele im Straßenverkehr lassen sich in Zukunft nur durch einen Antriebsmix aus optimierten Verbrennern, Hybriden und Elektrofahrzeugen erreichen. Bei den Verbrennungsmotoren sind neben Benziner und Diesel insbesondere auch synthetische Kraftstoffe (“E-Fuels”) eine Möglichkeit, Verbrennungsmotoren klimafreundlich zu machen. Bei den Hybriden ist neben dem Range Extender insbesondere der Plugin-Hybrid eine Option, mit der auch ein vollelektrischer Betrieb möglich ist. Bei den reinen Elektrofahrzeugen wird die Zukunft sowohl aus batterieelektrischen Fahrzeugen als auch Brennstoffzellen-Fahrzeugen bestehen, die mit Wasserstoff (H2) betrieben werden.

Im Luftverkehr ist CO2-neutrales Kerosin das Schlagwort

Im Luftverkehr ist ebenfalls noch ein weiter Weg zu gehen. Die CO2-Emissionen des Luftverkehrs machen knapp 3% der gesamten Emissionen aus, steigen aber jedes Jahr kontinuierlich um ca. 5%. Da Batterien im Flugzeug zu schwer sind, muss herkömmliches Kerosin durch einen regenerativen Kraftstoff ersetzt werden. CO2-neutrales Kerosin ist dabei das Schlagwort. Ein ökologisch sinnvoller Weg könnte ein strombasierter Kraftstoff sein, der im sogenannten „Power-to-Liquid“- Verfahren gewonnen wird. Mit großer Energiemenge kann Wasserstoff per Elektrolyse aus Wasser herausgelöst und dann mit Umgebungs- CO2 zu Kerosin weiterverarbeitet werden. Wird dieses verbrannt entsteht CO2, das zuvor der Umwelt entzogen wurde – ein klimaneutraler Kreislauf.

Ausbau des Schienennetzes, Stärkung der Bahn und massive Investitionen in den ÖPNV verändern den Modalsplit

Es ist allerdings abzusehen, dass es zusätzlich einer Entwicklung weg vom Kraftfahrzeug und Flugzeug bedarf. Dies ist zum einen über eine bessere Nachfragesteuerung nach Transport, z.B. der Vermeidung von Pendlerverkehren durch Home Office oder Behördensatelliten und Wegfall von Dienstreisen durch Videotechnik zu erreichen. Zum anderen muss eine Veränderung des Modalsplits dazu führen, dass Verkehr von der Straße (und der Luft) auf die Schiene und vom Individuum zu geteilten Verkehrsmitteln (z.B. ÖPNV, Car Sharing) verschoben wird. Der Ausbau des Schienennetzes, die Stärkung der Bahn und massive Investitionen in den ÖPNV müssen dazu führen, dass Wege sowohl in der Stadt als auch auf dem Land immer weniger im eigenen PKW zurückgelegt werden. Die Mobilität von morgen muss nachhaltig und geteilt sein.

How mobility & transportation can decarbonize without just taking symbolic action

29 June 2020It’s an old discussion with a lot of biased arguments being repeated continuously. What is clear: Climate change keeps progressing with global carbon dioxide emissions constantly increasing. To slow global warming down, carbon dioxide emissions need to be reduced fast and significantly.

The discussion evolves around symbolic actions

However, a huge part of the discussion on how to achieve this goal does mainly evolve around more or less symbolic actions without any major impact. This is especially true for the transportation and mobility sector. Limiting long-distance air travel, prohibiting domestic flights, introducing speed limits, just to name a few of these actions supposedly saving our planet. Everybody even only having a rough idea about the facts and numbers can see the flaw. Having a look at the global carbon footprint, we realize that the aforementioned measures will only have a very minor, sometimes not even measurable impact. Just to make it clear: These actions won’t save the climate!

Why not? And how can our measures achieve a maximum impact? What are the major levers for carbon dioxide reduction?

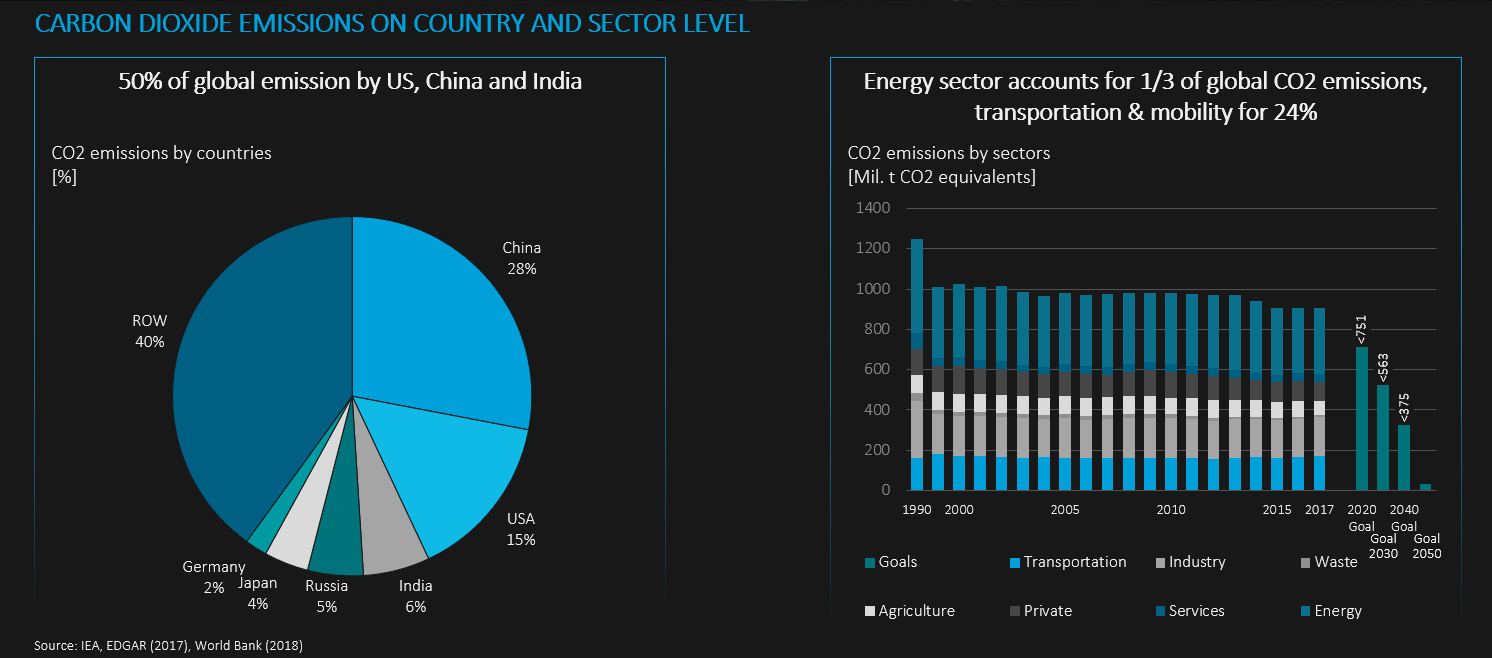

Country and sector views reveal the major levers

To identify the major levers, we should have a look at the situation from two angles. On a country level, around 50% of global emissions are caused by the United States, China and India only. On a sector level, the energy sector causes about 1/3 of emissions. Transportation and mobility accounts for about 24%. Further detailing these emission, road vehicles emit 18%, air travel and ships both emit about 2.5%, 1% are caused by other means of transportation (e.g. rail).

Carbon dioxide emissions on country and sector level

Countries with the largest emissions in transportation are the United States, China, Russia and India. And the emissions are expected to increase in the future, especially with emerging countries in Asia whose transportation sectors are growing rapidly. These numbers make clear how insignificant measures like prohibiting domestic flights in France or introducing a speed limit in Germany are in the global context. The impact won’t even be measurable.

There are two different approaches to address CO2 reduction taking into consideration the sector and country level view.

Leveraging mobility technology and innovation

On sector level, we need to leverage technology and innovation. This means that we need to develop green, carbon-neutral technologies and innovations. In the transportation and mobility field, climate-neutral technologies can be battery technology for electric cars, hydrogen-based fuel cells for trucks and aircrafts, alternative fuels for conventional cars with internal combustion engine. Moreover, we need to fully electrify our public transport (e.g. electric buses) and at the same time enhance digitalization and multi-modal mobility to push shared modes such as car and ride sharing connected with and to our public transport.

If we manage to make these technologies not only carbon-neutral but also economically beneficial, then other countries will also adopt them. Even if they only doi it to save cost. The economic argument is an important one since otherwise we cannot make sure that major emitting industry nations and emerging countries are following our decarbonization approach.

By focusing our R&D efforts on these technologies, their positive climate impact can be leveraged across countries and is not restricted to only limited geographies (e.g. Europe). An even further step could include an open source approach. Being driven by a higher cause and being open-minded, our companies owning property rights such as patents could make their technologies and innovations available to the public on a global scale. This would further increase the speed of change.

Investing with maximum impact per Euro spent

It is clear that stopping climate change can only work pursuing an international approach. Therefore on a country level, we need to invest money where the impact on carbon dioxide reduction for each Euro invested is the highest. Usually, money invested in developing countries results in much higher carbon dioxide reductions than the one invested in developed regions such as Central Europe. In an extreme case, not switching off an efficient coal-fired power station could be a rational choice. Instead of investing in expensive green energy options to replace the efficient coal-fired plant in Europe, replacing an old coal-fired power station in Africa by a modern one can have a higher CO2 effect per Euro invested. It is key to leave a primarily country-based view and allocate resources globally to generate the highest carbon dioxide reductions.

The benefits of this approach are twofold. By moving away from symbolic actions just for our peace of conscience, we focus on measures with real impact. And thinking of our (European) economy, we develop the technologies of the future to export globally and to guarantee our wealth, strengthen our social welfare and create meaningful jobs.

The Best Podcasts from Mobility, Transportation & Automotive

14 May 2020If you are interested in new mobility topics, you might know that there are plenty of mobility and transportation podcasts out there. With mobility being such a vast space that is interconnected to public transportation, urban planning, the sharing economy and automotive, podcasts are a great way to stay up-to-date. So here is a brief overview on my personal favorite podcasts in the mobility field.

Shift Mobility Podcast

Shift Mobility Podcast

Shift is the mobility-focused podcast from Automotive News. It broadly covers the future of transportation with topics such as sharing services, autonomous driving, new automotive business models or smart city. Hosts Pete Bigelow and Leslie Allen usually welcome leading mobility experts from North America. Shift is also a leading magazine in the automotive and mobility industry.

Digital Kompakt: Automotive Mobility Podcast

Digital Kompakt: Automotive Mobility Podcast

The Automotive Mobility Podcast focuses on the CASE topics, namely connected, autonomous, shared and electrified mobility in Germany. The guests are industry experts from German mobility companies. Patrick Setzer with his major industry experience (e.g. BMW, Lufthansa) does a great job of moderating the talks in an informative and competent way. The podcast is integrated in the Digital Kompakt label that is promoted in the advertising sections.

Fully Charged

Fully Charged is a UK-based clean energy & electric vehicle site featuring blogs, vlogs, shows and podcasts on electric cars. It provides plenty of information on electric mobility and the podcast episodes feature numerous industry experts. It is hosted by writer and broadcaster Robert Llewellyn who discusses a broad range of topics in the field of sustainability.

The Mobility Podcast

The Mobility Podcast features a broad scope of transportation and technology discussions. Typical topics in the mobility space are micromobility, autonomous vehicles and Mobility-as-a-service (MaaS). The guest list is quite international with thought leaders from mobility companies. The podcast is run by Greg Rogers, Gregory Rodriguez and Pete Gould who have strong backgrounds in politics, law and consulting.

Reinventing Transport

Reinventing Transport is a podcast by Paul Barter, an Australian transport-policy researcher. Its common theme is Urban Mobility with talks on parking or transportation case studies of showcase cities such as Singapore. Paul likes to talk to various transport experts and sometimes does episodes only featuring himself. With “Reinventing Parking” he offers a second podcast.

The War on Cars

The War on Cars

The War on Cars podcast contrasts the automobile on one and the city on the other side. Activity-based modes like cycling or walking are major topics. The guest list includes writers, media officials and TV hosts to discuss the latest developments in urban transportation. The podcast is hosted by Doug Gordon, Sarah Goodyear and Aaron Naparstek who are located in New York City.

I admit that this is a very subjective selection and I know that there many other great podcasts in the mobility, transportation and automotive space. Let me know which ones are your favorites and why in the comment section below!

Covid-19: Do we need to restrict our mobility?

05 May 2020The Covid-19 pandemic has sent many countries into a state of shutdown where major parts of public life came to a halt. The virus is obviously threatening public health and the lives of many people. Globally, we must expect hundreds of thousands of deaths caused by Covid-19.

At the same time, each year more than one million people die in accidents related to mobility and traffic. Based on WHO numbers, the annual number of traffic deaths is about 1.35 million. So far not a single country has imposed measures similar to the Covid-19 shutdown restrictions in the mobility field. Do we need to fight traffic accidents with the same rigorousness as we fight Covid-19?

Moving from a fear-based to a fact-based approach

To understand the Covid-19 measures that have been imposed, we need to have a look why these drastic measures have been implemented in the first place. The goal of the measures was to contain the virus in order to not exceed the capacity of the health system. Extending intensive care unit (ICU) capacities, the goal of preparing hospitals for a dramatic wave of Covid-19 patients could be achieved in countries such as Germany, Austria or Scandinavia. In Italy, Spain and France however, even more drastic measures including curfews for several weeks could not prevent the health system from being overwhelmed. In contrast, several Asian countries such as South Korea or Taiwan didn’t even need a public shutdown to mitigate the crisis smoothly. Therefore, the shutdown is obviously not a decisive factor or the best measure at hand to deal with the crisis. A shutdown is buying time but is not a sustainable strategy in itself.

Triggered by images of trucks carrying dead bodies in Northern Italy, the public discussion has been an emotional and fear-based one. To put the measures in perspective, a rather rational and fact-based approach is required. And the facts do clearly suggest a smart and more differentiated strategy.

Flawed statistics but a well-defined risk group

It has been widely discussed that the official statistics are flawed. The reported number of deaths is generally too high because a significant amount of infected people dies with the virus inside but not necessarily due to the virus. The reported number of confirmed infections is way too low because it depends on the amount of testing and does not include infected people that have not been tested. Hence the perceived case fatality rate (# of reported deaths divided by # of confirmed infections) is overestimated. Studies suggest an infection fatality rate of 0.3-0.4% based on actual infections.

Even more interesting is the risk group. The average age of deaths has been around 80 and almost exactly corresponds to the average life expectancy, even when considered for each gender individually. In some countries like Germany, even at the peak of the pandemic there is no excess mortality compared to the average mortality. Experts predict that most countries won’t see any excess mortality when considering the entire year.

Moreover, 50% of deaths have been diagnosed with pre-existing conditions. Less than 1% of deaths did not have pre-existing illnesses. Case fatality rate for infected people without pre-existing conditions is 100 times lower than with pre-existing conditions. Compared to the flu, the case fatality rate for the group with no pre-existing conditions is way lower for Covid-19.

Three types of appropriate measures

With the well-defined risk group the appropriate measures in general and for the mobility sector are at hand. First, the risk groups need to be protected. This has nothing to do with confinement or isolation. It is a recommendation for people in the risk group to voluntarily limit their potential exposure to the virus. People outside of the risk group have a very low risk of severe health problems and can responsibly resume economic activity including mobility and travel. This smart and differentiated approach needs to be supported by personal hygiene (hand washing etc.) and physical distancing measures that have already been widely in place during the pandemic.

Mobility and travel enhance quality of life and create opportunities

The aforementioned measures make sure that mobility and travel will be possible in the near future. The imposed shutdowns were a temporary action to contain the virus. After this initial phase of containment to prevent the collapse of health systems, they cannot be maintained. Maintaining the shutdown would mean a too narrow focus not taking into account other health, social or economic considerations. In the same logic, restricting mobility to prevent traffic deaths would mean a one-sided focus on safety without considering the negative imapcts of limited or no mobility.

The comparison between the deaths by the pandemic and the deaths by traffic accidents makes clear that an extended duration of shutdowns is socially inadequate. Mobility needs to be possible. It is a major driver of the welfare of societies and does enable health systems to function properly. It creates opportunities for the individual. In this respect we are implicitly accepting the negative impacts of both the pandemic and mobility. Neither a one-sided focus on health nor freedom of mobility can be an adequate approach.

Mobility and Travel in Post-Corona

15 April 2020The Corona pandemic has caused huge disruptions in travel and mobility. Borders have been closed, travelling has come to a halt, aircrafts are grounded. Urban public transport and long-distance trains are experiencing a reduction in passenger numbers of up to 90%. Car and ride sharing companies are radically limiting their activities or even stopping their operations. Micromobility operators such as kickscooter companies cease offering their services in most cities, entire countries or even continents. That’s happening right now. But what will happen after the Corona dust has settled? There will be no back to the old normal, many experts believe. But is that really true?

Mobility and travel will resume after the crisis

Yes, there are some major implications by the current pandemic. In the short-term, individual transport is gaining market share, public transport is suffering. Due to social distancing, travelling by one’s car seems beneficial right now. But owning a car is also a cost factor in times that are and will be financially challenging for many of us. And the drawbacks of cars remain. Pollution, congestion and traffic accidents will still be there when travel and mobility picks up again after the crisis. And public transport will still be the backbone of mobility, at least in urban areas. Yes, there will be less public transport during a transition period. But after mass immunization and/or vaccination has occurred, public transport capacity and utilization will return to previous levels. Besides a few exceptions, in the long-term no dramatic changes are expected. One trend that will remain though are remote work schemes with home office and video conferencing. These schemes had long time been identified as a demand management lever to reduce inefficient daily commuting. If the crisis has pushed remote work schemes to new popularity levels, that’s a positive impact for sure.

Air travel will be hit by a supply shortage

Yes, the air travel industry is hit hard by the crisis. And we can expect that some airlines (e.g. Norwegian) will be in severe trouble and will not make it out of the crisis. At the same time, most major airlines such as Lufthansa or Singapore Airlines will be saved by their governments. Financial aid, debt guarantees and even acquiring major stakes in their most important airlines will be the strategies many governments adopt to save their countries’ main carriers.

This might also be true for airport operators and ground service providers (e.g. baggage handling) who have seen a decline in passengers of more than 95%. For an infastructure business that is primarily fixed-cost based, this is a disaster.

The Corona air travel distaster

Most airlines will be smaller after the crisis than before. Less employees, fewer and smaller aircrafts and less travel destinations. Therefore, supply for flights will decrease. Regarding consumer demand, there will be a rather slow ramp-up in air travel after the crisis. But in the end people will again be travelling to a similar extent as before the crisis. With flight demand slowly but continuously picking up, consumer prices could go up. This development is in line with policymakers’ goal to make flight tickets more expensive for sustainability (e.g. carbon dioxide emissions) reasons. In the business segment things look different. Due to increased video conferencing, there should be significantly less business travel demand in the post-Corona future.

The consolidation in smart mobility is accelerated

Yes, it is obvious that sharing concepts such as car or home sharing (Airbnb etc.) are heavily affected by the pandemic. Nevertheless, the sharing economy is well-established and with a few adjustments, the overall concept will remain. We will see that financially strong platforms or corporate-backed players such as Uber or Your Now will defy the crisis. Smaller players in need of funding, however, might be in trouble. Venture capital is hard to get in Corona times and the consolidation in the shared mobility space will accelerate. Especially ride sharing providers offering shared rides with multiple passengers will be having a hard time in the shared mobility end game.

Yes, the same is true for the micromobility industry. Micromobility is an individual mode of transportation and will be an important component in future mobility. Kickscooters have recently been a hype to fill the first- and last-mile gap. But a long winter followed by a tough Corona spring made operators suffer. Kickscooter providers such as Voi, Lime and Bird have disappeared from many cities. And it is not yet clear who will return. Just as in the shared mobility space, the pandemic will accelerate the necessary industry consolidation.

In the future, kickscooters could be more and more replaced by activity-based transportation modes. Cycling and walking are more popular than ever. In many cities bike sharing and cycling lanes are heavily pushed by policymakers. Some cycling lanes established during the current crisis might persist and replace roads that have been used by cars before.

The long-term trends are still in place

In a nutshell, the post-pandemic mobility future will probably not be that different. The long-term trends towards sustainable, shared and smart, digitally enabled mobility are still in place. With the crisis left behind, the willingness to assess alternatives to traditional mobility modes may well increase. Smart mobility can provide solutions to increased social distancing and commuters turning to increasingly varied and disparate transportation options. The current crisis will be a driver and accelerator of the smart mobility movement.

The Mobility of the Future – Showcase Singapore

30 March 2020When it comes to examples for how the mobility of the future might look like, Singapore has been stated as showcase for a smart mobility vision.

Singapore’s vision is the “car-lite” city

Having a share of around 67% in public and shared transportation, Singapore’s modal split is already showing a smart and sustainable mobility approach. This means that 2/3 of its urban travel is based on train, bus and taxi. Only about 1/3 of Singapore’s transport are private modes such as car and motor bike.

Working towards its vision of a “car-lite” city, Singapore’s government has established several measures that make private cars rather costly and less attractive. A strict vehicle quota limits the number of cars. Road pricing increases the cost of private car usage. And the tax system further imposes financial burden on car owners. By doing so, Singapore is proactively fighting congestion, pollution and car accidents.

The technocratic administration pushes non-motorized modes

The data-driven, technocratic government has a key role in shaping Singapore’s mobility of the future in the long term. Using data and scenarios in a non-democratic but rigorous, transparent and efficient way , the Singapore administration is further pushing sustainable transportation options focusing on non-motorized modes. The public transportation system based on urban rail (MRT) connects the city centre and the suburbs. It is constantly expanded and improved. Active mobility modes such as walking and cycling are underrepresented but pushed strategically, e.g. by building showers and lockers at mobility hubs such as bike stations. Roads are redesigned to be more pedestrian-oriented and cyclist-friendly. Recently added micro-mobility options such as e-scooters and kick scooters do further contribute to the reduction of individual motorized transport.

Autonomous driving to address lack of labor and land

With its ageing population sometimes referred to as “silver tsunami”, Singapore authorities are not banning cars entirely. They are rather working towards a future based on electric and especially autonomous cars. Numerous pilots for self-driving shuttles or buses have been established. Autonomous driving is seen as a potential to use roads more efficiently in a country that is notorious for its land shortage. Moreover, self-driving buses are a solution to Singapore’s lack of labor for operating public transport.

Mobility-as-a-service with public and shared transport as core

Overall, the government is pursuing a vision that could be described as a seamless mobility approach. Singapore’s mobility of the future will be a door-to-door, on-demand, multimodal service where private, shared and public transport are all interconnected. It is the concept of Mobility-as-a-service (MaaS) that delivers a mobility solution rather than only transport. At its core will be public and shared transport (MRT, bike/ car/ ride sharing etc.) based on smartphone apps that guarantee individual and hassle-free first-and-last-mile connectivity. MaaS Global is a good example for bringing the vision of seamless mobility to Singapore. With their Whim mobile app, the Finnish startup plans to combine numerous modes of transport, from train, bus to taxis, car sharing and bikes in just a single app.

A key success factor for mobility in Singapore is the transportation system being planned and monitored by a strong administration that cooperates with innovative startups in public-private partnerships. While the administration provides anonymized traffic data, the startups bring the latest technology to the table. This smart government action is in strong contrast to many Western governments whose inefficient administrations do still focus on extensive private car usage and fail to consistently develop public and shared transportation.

My Favorite Mobility Blogs

26 March 2020If you are interested in the future of mobility, you are constantly in search of well-researched and up-to-date information. A good way to find this type of content are blogs. You have probably realized that there are plenty of mobility and tranportation blogs out there. Here are my top picks that I highly recommend.

Human Transit

Human Transit

This is the blog of public transit consultant Jarrett Walker. It focuses on urban mobility and public transport in North America. Jarrett tries to put into perspective the design of public transit and its underlying goals. It’s a great resource for everything related to public transport and commuting.

Streetsblog

Streetsblog is a daily new site discussing how to reduce dependence on cars and push alternative modes such as walking, biking, and public transit. It focuses on urban planning and mobility in the US. The blog’s goals are to prevent pedestrian injuries, build out bicycle networks, and make transit more useful. It also offers numerous videos and a podcast.

![]()

Zukunft Mobilität

This mobility blog in German language covers pretty much all topics on future mobility. Public transport, air travel, CASE technologies, urban mobility and infrastructure. Author Martin Randelhoff has been blogging about urban transport and mobility for many years and has been featured on German media. If you speak German, that’s the blog to go to!

![]() Ecomobility

Ecomobility

EcoMobility is an ICLEI initiative which is a global network of local and regional governments committed to sustainable urban development. Their goal is to achieve sustainable mobility through policies, planning and implementation. Their resources include articles on public transport, urban freight and emerging mobility trends from electric to shared mobility.

![]() The Urban Mobility Daily

The Urban Mobility Daily

The Urban Mobility Daily is a Paris-based initiative connected to the yearly Autonomy & Urban Mobility Summit. Their content focuses on new mobility topics such as electrification, sharing or Mobility-as-a-service in France and the European Union. It is also open for content contributions.

Mobilitätsmarkt – die Musik spielt nicht bei uns

25 November 2019Wenn wir in Deutschland über die Mobilität der Zukunft diskutieren, dann reden wir meist über Deutschland – und vielleicht ein bisschen Europa. Dabei sind der deutsche oder europäische Mobilitätsmarkt in einer globalen Perspektive gar nicht so bedeutend wie man vielleicht denkt. Nicht beim heutigen Volumen und schon gar nicht beim zukünftigen Wachstum. Davon gleich mehr.

Die Mobilität der Zukunft ist nachhaltig, integriert, geteilt und digital

Bevor wir in die Märkte einsteigen, noch eine kurze Überlegung, wie die Mobilität der Zukunft optimalerweise aussehen sollte. Kurz gesagt, sie ist nachhaltig, integriert, geteilt und digital.

Nachhaltig im Sinne von klimafreundlich, insbesondere im Hinblick auf CO2-Emissionen. Integriert im Sinne von gesamthaft („end-to-end“) gedacht, als multimodale Mobilität zwischen A und B unter Verknüpfung verschiedener Verkehrsmittel. Geteilt im Sinne einer Auslastungsoptimierung der Verkehrsmittel weg vom Privatbesitz (Auto, Fahrrad etc.) hin zu Sharing-Ansätzen (z.B. Car Sharing, Bike Sharing etc.). Und digital unterstützt, mit dem Smartphone als dem persönlichen Reisebegleiter.

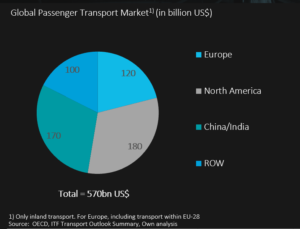

Der globale Mobilitätsmarkt ist 600 Milliarden US-Dollar schwer

Nach diesem Verständnis ist Europa mit Sicherheit der reifste Markt, Nordamerika hinkt hinterher und in Asien passiert das zukünftige Wachstum. In unserer groben Abschätzung des globalen Mobilitätsmarkts haben wir uns den Personenverkehr in Europa (EU), Nordamerika (USA und Kanada), und Asien (China und Indien) angeschaut. Alle übrigen Länder und Regionen sind im Cluster ROW („Rest of World“) zusammengefasst und beinhalten vor allem Südamerika, Südostasien und Afrika. Die betrachteten Verkehrsmodi umfassen PKW, Flugzeug, Zug und Bus.

Globaler Mobilitätsmarkt in Milliarden USD

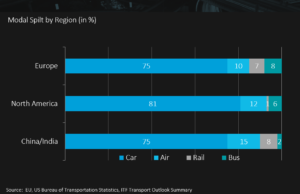

Mit einem Volumen von ca. 600 Milliarden US-Dollar ist der globale Markt für Mobilität riesig. Schaut man sich die Regionen an, gibt es erhebliche Unterschiede im Hinblick auf Wachstum, Reife, Mobilitätsbewusstsein und Modalspilt. Der Anteil des PKW ist mit mehr als 75% in allen Regionen extrem hoch, wird aber insbesondere in Europa abnehmen. Trotz der in manchen Regionen aufkommenden “Flugscham” ist der Luftverkehr weiterhin zunehmend mit einem Anteil von ca. 10-15% an der Gesamtmobilität. Die vergleichsweise klimafreundlichen Varianten Zug und Bus sind bisher noch deutlich unterrepräsentiert. Die größten Unterschiede zwischen den Regionen zeigen sich bei Wachstum, Reife und Mobilitätsbewusstsein.

Modalsplit nach Regionen

Europa reif, Nordamerika verspätet und Asien heterogen

In Europa gibt es aufgrund des zunehmenden Bewusstseins für Klimaschutz und die entsprechende EU-Gesetzgebung (z.B. CO2-Flottengrenzwerte für die Autoindustrie) eine Tendenz weg vom Auto hin zu Bus und Bahn. Beide Verkehrsmittel sind vergleichsweise klimafreundlich, gemäß verschiedener Analysen von Emissionswerten der Fernbus sogar noch mehr als die Bahn. Während das Auto ungefähr 140 Gramm Treibhausgasemissionen pro Personenkilometer ausstößt, kommt der Zug im Fernverkehr in Deutschland auf 36 Gramm, der Fernbus sogar auf nur 32 Gramm. Das Flugzeug als Klimakiller liegt bei ca. 200 Gramm. Dieses aufkommende Klimabewusstsein lässt vor allem in europäischen Großstädten das Angebot und die Nutzung von multimodaler Mobilität und von Sharing-Konzepten wachsen.

Anders ist die Situation in Nordamerika, insbesondere den USA. Fehlende Klimaregulierung und die geographische Struktur führen zu hohen Anteilen von PKW und Flugzeug. Bus und Bahn spielen fast keine Rolle. Die Transportmittelwahl ist in weiten Teilen der USA eine binäre. Alles was noch mit dem Auto machbar ist wird gefahren, der Rest wird geflogen. Bis auf einige Großstädte sind multimodale Mobilitätskonzepte wenig verbreitet.

Der asiatische Markt ist sehr heterogen, gemein ist allen Märkten lediglich die hohen zu erwartenden Wachstumsraten, besonders auch in der Luftfahrt. Bis 2050 werden China und Indien ein Drittel des gesamten globalen Personenverkehrsaufkommens ausmachen. Dabei ist China geprägt durch eine große Offenheit und auch ausgeprägte Zahlungsbereitschaft für smarte, digitale Mobilität. Diese wird insbesondere durch ein großes Vertrauen in chinesische Digitalunternehmen wie z.B. Baidu oder Didi unterstützt. In Indien ist ein weiteres Wachstum der Luftfahrt zu erwarten, der Bus ist deutlich unterrepräsentiert. Die anderen asiatischen Märkte (z.B. Südostasien) sind extrem heterogen, mit hohem Wachstum aber teilweise auch mit begrenzter Digitalisierung wie z.B. der Durchdringung von Onlinebuchungen.

Nachhaltige Tür-zu-Tür Lösungen sind gefragt

Für europäische Mobilitätsanbieter mit Wachstumsambitionen lassen sich daraus mehrere Implikationen ableiten. In Europa ist eine Positionierung als nachhaltiger, multimodaler Mobilitätsanbieter anzustreben. Transparenz über Nachhaltigkeit bei CO2-Emissionen der angebotenen Mobilitätsoptionen ist dabei von hoher Bedeutung. Um dem Kunden eine gesamthafte Tür-zu-Tür-Lösung anbieten zu können, wird die Integration der letzten Meile entscheidend sein, insbesondere auch außerhalb der Ballungszentren. Und für „bold moves“ außerhalb Europas führt kein Weg vorbei an China, auch wenn der Marktzugang reglementiert und mit zahlreichen Fallstricken behaftet ist.

Klimaschutzpaket – wer hat sich das ausgedacht?

24 September 2019Seit der Vorlage des Klimaschutzpaketes durch die Bundesregierung vergangenen Freitag gibt es in der öffentlichen Diskussion laute Kritik an dem geplanten Maßnahmenbündel. Häufig gehörte Kritikpunkte bezeichnen das Paket wahlweise als zu langsam, zu teuer, zu mutlos, zu planwirtschaftlich, innovationsfeindlich oder als kleinster gemeinsamer Nenner. Dabei ist es eigentlich sogar noch schlimmer. Im Realitätscheck stellt man schnell fest, dass zahlreiche Maßnahmen im bunten Klimaschutzblumenstrauß nicht nur unzureichend, sondern sogar kontraproduktiv in die entgegengesetzte Richtung hin zu mehr Kohlenstoffdioxidausstoß steuern.

Wir wollen nachfolgend einige Beispiele der offensichtlichen Fehlsteuerung im Verkehrssektor geben, der die Zukunftsthemen Mobilität, Transport und Verkehr beinhaltet.

Unwirksame Steuerung: CO2– Preis und Kfz-Steuer

Der grundsätzlich richtige Ansatz einer CO2-Bepreisung wird konterkariert durch die homöopathische Dosierung und eine fehlende Mengenbegrenzung. Zunächst ist der Einstiegspreis von 10 Euro pro Tonne CO2 (und selbst dieser erst ab 2021) bei weitem zu niedrig, um spürbare Wirkung zu entfalten. Ziel einer CO2– Bepreisung ist es, in allen Wirtschafts- und Lebensbereichen und gerade auch im Verkehrssektor eine Lenkungswirkung hin zur Einsparung von CO2 zu erzielen. Insbesondere bei Unternehmen der Mobilitätsbranche (Automobil, Transport, Verkehr) soll die Bepreisung eine Lenkungswirkung bei Technologien, Innovationen und grundsätzlich allen Investitionsentscheidungen erzielen. Dies wäre allerdings erst ab einem CO2-Preis von ca. 35-40 Euro pro Tonne zu erwarten. Noch entscheidender ist, dass das vorgeschlagene Modell eines (langsam ansteigenden) Festpreises für CO2 wie eine Steuer wirkt, nicht wie ein Preis. Für eine marktwirtschaftliche Bepreisung mit Lenkungswirkung müsste die Gesamtmenge an CO2, die bis zu einem bestimmten Zeitpunkt noch ausgestoßen werden darf, konkret festgelegt werden. Die dadurch festgelegte Menge könnte dann gehandelt werden und es würde sich der marktwirtschaftlich faire Preis bilden, dessen Wirkungen ggf. über Preisunter- bzw. Preisobergrenzen abgefedert werden könnten. Das aktuell vorgeschlagene Modell ist davon und von der angestrebten Verhaltensänderung aller Akteure weit entfernt.

Ähnlich unwirksam ist die sog. CO2-bezogene Reform der Kfz-Steuer, die die Bemessungsgrundlage der Kfz-Steuer hauptsächlich auf die CO2-Emissionen pro km bezieht. Was gut klingt, ist nicht zu Ende gedacht. Eine höhere Steuer spart nämlich zunächst kein einziges Gramm CO2 ein. Entscheidend ist ja die Nutzung des jeweiligen Fahrzeugs. Mit anderen Worten: ein 2,5t schweres SUV, das nur zu Statuszwecken gekauft wird und wenig fährt, stößt weniger CO2 aus als ein sparsamer Kleinwagen, der aber hunderte von Kilometern jeden Tag, z.B. zum Pendeln gefahren, wird. Womit wir bei der Pendlerpauschale sind, der Mutter aller Fehlsteuerungen.

Kontraproduktive Steuerung: Pendlerpauschale

Bei der Pendlerpauschale ist nicht zuletzt durch ein Interview des Grünen-Vorsitzenden Robert Habeck eine Diskussion entbrannt, in welchem Fall welcher Berufspendler welchen Betrag erhält. Nur wenn er Auto fährt oder auch wenn er Bahn fährt? Und bringt es auch der Krankenschwester etwas, die ohnehin immer nur pauschal in der Steuererklärung ihre Werbekostenerstattung beantragt? Bei diesen Randdiskussionen wird komplett vergessen, dass die Pendlerpauschale sowohl ökonomisch als auch ökologisch völlig falsche Anreize setzt. Hier wird Pendlern Geld dafür bezahlt, dass sie die Distanz zwischen ihrem Wohn- und Arbeitsort maximieren. Wer kann sich sowas ausdenken? Zum einen wird die Überlastung unserer Verkehrssysteme (Straßen, ÖPNV etc.) weiter gefördert und der volkswirtschaftliche Schaden von Zeitverlust im Stau ist schon heute immens. Zum anderen wird der Ausstoß von CO2 (z.B. durch Pendeln mit dem eigenen PKW) weiter belohnt und der Effekt der CO2-Bepreisung sogar überkompensiert. Sinnvoll wäre statt der Erhöhung die Abschaffung der Pendlerpauschale, um im Sinne einer intelligenten Nachfragesteuerung Anreize für weniger pendeln und kurze Strecken zu setzen. Auch wenn es viele nicht glauben, sowohl Arbeits- als auch Wohnort sind in unserer freien Gesellschaft frei wählbar.

Verschwendung von Steuergeld bei Aushebelung der Marktwirtschaft

Abschließend noch einige Beispiele für Maßnahmen aus dem Klimaschutzpaket, bei denen der Schaden für das Klima zumindest gering ist, dafür aber einfach Steuergelder verschwendet werden.

Der Bund wird in den nächsten zehn Jahren jeweils 1 Mrd. Euro an Eigenkapital für die Deutsche Bahn zur Verfügung stellen. Ziel ist die Modernisierung des Bahnsystems. Es wird nur leider vergessen, dass Bahnsystem ungleich Deutsche Bahn und der Staat kein guter Unternehmer ist. Es ist nur schwer nachzuvollziehen, wohin die Gelder genau fließen und es ist zu erwarten, dass die DB sich durch die Staatsspritze unlautere Vorteile gegenüber der privaten Konkurrenz verschaffen wird.

Die Etablierung von Modellprojekten für ÖPNV-Jahrestickets zu 365 Euro ist zwar gut gemeint, aber nicht wirklich hilfreich. Zum einen sind die meisten ÖPNV-Systeme in Deutschland zu Stoßzeiten ohnehin überlastet und es bräuchte zunächst mal einen Ausbau der öffentlichen Infrastruktur. Zum anderen sind ÖPNV-Systeme in Deutschland bereits heute massiv steuersubventioniert. Eine weitere Umverteilung der Lasten von den Nutzern zur Allgemeinheit ist nicht angebracht. Oder soll der gut verdienende Unternehmensberater ohne Auto in Berlin-Mitte sein ÖPNV-Ticket jetzt auch noch von der Allgemeinheit finanziert bekommen?

Zur Förderung des Automobilsektors und der gesamten Wertschöpfungskette der Elektromobilität in Deutschland und Europa, wird die Ansiedlung von Batteriezellfabriken mit 1 Mrd. Euro subventioniert. Erst kürzlich wurde die stark umstrittene Entscheidung für den Standort Münster gefällt. Ein ähnliches Unterfangen ist vor Jahren bereits bei der Subventionierung der deutschen Solarindustrie gescheitert, Milliarden an Steuergeldern waren weg. Wir haben die Analogien bereits an anderer Stelle diskutiert.

Es bleibt damit die Hoffnung auf das Monitoring. Die Fortschritte bei der CO2-Einsparung sollen jährlich genau ermittelt und durch einen externen Expertenrat validiert werden. Die bereits heute abzusehenden, notwendigen Anpassungen sollten im Interesse des Klimas besser früher als später erfolgen.

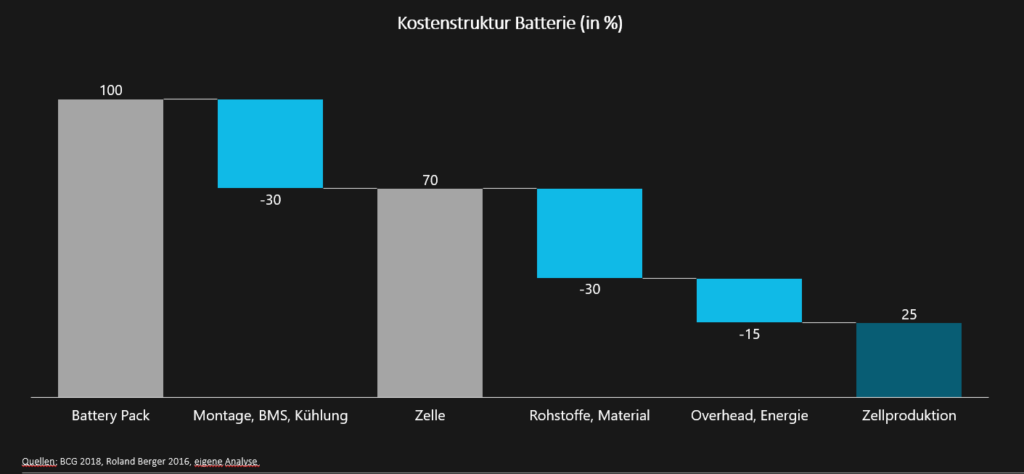

Deutsche Batteriezellproduktion – das nächste Milliardengrab?

24 May 2019Volkswagen hat den Strategieschwenk auf Elektromobilität vollzogen und will bis 2025 drei Millionen Elektrofahrzeuge pro Jahr verkaufen. Zusätzlich wurde jetzt der Einstieg in die Zellfertigung verkündet. VW investiert eine Milliarde und baut eine eigene Zellproduktion auf. Der Fokus soll dabei auf Festkörperbatterien liegen, die aber wohl nicht vor 2030 in Serie gehen könnten. Gleichzeitig wurden langfristige Lieferverträge über die Lieferung von Batterien in Milliardenhöhe abgeschlossen. Konkurrent Daimler kauft Batteriezellen im Wert von 20 Milliarden Euro, der Fokus der eigenen Wertschöpfung soll aber weiterhin auf dem Batteriemodul („Battery Pack“) liegen, eine eigene Zellproduktion soll vorerst nicht aufgebaut werden.

Gleichzeitig wird die deutsche Bundesregierung massiv den Aufbau einer europäischen Batteriezellfertigung unterstützen. Insgesamt sollen 1,7 Milliarden Euro in die Förderung des Aufbaus einer Batteriezellfabrik fließen. Die Bundesregierung will bis zum Jahr 2021 eine Milliarde Euro für die Herstellung von Batteriezellen für Elektroautos bereitstellen. Frankreich legt weitere 700 Millionen Euro in den Fördertopf. Ziel der Förderung ist neben der Schaffung von Arbeitsplätzen insbesondere die Schaffung einer nachhaltigen, grünen Batteriezellproduktion.

Aber machen Subventionen für eine deutsche Zellproduktion überhaupt Sinn? Oder gibt es ein Ende mit Schrecken wie bei der Solar-Förderung? Trotz Übermacht der chinesischen Hersteller wurden der deutschen Solarindustrie immense Subventionen in Milliardenhöhe gewährt. Es entstanden massive Überkapazitäten, die die Preise für Solar-Panels zwischen 2006 und 2015 um ca. 50% sinken ließen. Mehr oder weniger alle deutschen Hersteller wie z.B. Solarworld oder Q-Cells gingen pleite und die steuerfinanzierten Subventionen gingen dann meist an asiatische Hersteller.

Tatsächlich sind auch bei der Batteriezellproduktion erhebliche Zweifel angebracht, ob deutsche Steuergelder sinnvoll in eine Branche investiert werden sollen, die in Deutschland bisher praktisch nicht existent ist. Zahlreiche Gründe sprechen gegen eine europäische Zellproduktion.

Begrenzte Wertschöpfung bei niedrigen Margen

Zunächst mal macht es Sinn, sich die Wertschöpfung bei einem Elektrofahrzeug anzuschauen. Ja, es ist richtig, dass ca. 35% der Kosten eines Elektrofahrzeugs im Battery Pack liegen. Weitere 15% liegen beim Elektromotor und der Leistungselektronik, die restlichen 50% der Kosten sind nicht antriebsbezogen. Schaut man sich nun den Battery Pack gesamthaft an, sind 30% der Kosten auf Pack-Ebene und umfassen Montage, Batteriemanagementsystem (BMS) und Kühlung. Dieser Teil der Wertschöpfung wird meist bei den Automobilherstellern bzw. Tier 1-Lieferanten erbracht und ist nicht Teil einer Zellproduktion. Weitere 30% der Kosten sind Materialkosten und müssen im Fall einer eigenen Zellproduktion von Vorlieferanten bezogen werden. Zieht man von den restlichen 40% noch Energie- und Overheadkosten ab, bleiben nur ca. 25% eigentliche Produktionskosten (z.B. Lohn, Logistik, Invest), die im Rahmen einer Zellfertigung tatsächlich adressiert werden (s. Abbildung).

Kostenstruktur Batterie

Die aktuellen Prognosen gehen von einem massiven Ramp-up und einer hohen Überproduktion von Batteriezellen bis 2021 aus, was die Preise und Margen von Batteriezellen für Elektrofahrzeuge erheblich unter Druck setzen wird. Somit wird der Aufbau einer Zellproduktion zu einem Invest in eine Industrie mit begrenzter Wertschöpfung (ca. 25% des Battery Packs) und niedrigen Margen.

4-5 Jahre für den Aufbau einer deutschen Fertigung

Aktuell sind die führenden Zellhersteller wie Panasonic oder CATL ausschließlich in Asien verortet. Der Aufbau der Kompetenzen und der Produktionsanlagen einer deutschen Fertigung würde ca. 4-5 Jahre dauern. Neben der zeitlichen Herausforderung muss am Standort Deutschland zusätzlich mit Nachteilen bei Lohn- und Arbeitskosten gegenüber den asiatischen Herstellern gerechnet werden.

Ferner ist langfristig mit einer Angleichung der technischen Eigenschaften von Fahrzeugbatterien auf Zell- und auch Modulebene zu rechnen. Die Batterie wird sich daher voraussichtlich nicht als Differenzierungsmerkmal im Wettbewerb eignen. Eher werden Batteriezellen ein Massenprodukt sein, das als „Commodity“ am Weltmarkt bezogen werden wird.

Schließlich stellen die jetzt diskutierten Fördermaßnahmen in gewisser Hinsicht eine Abkehr von der Technologieoffenheit dar. Es ist unklar, ob sich das batterieelektrische Fahrzeug als führende Technologie nachhaltig wird durchsetzen können. Langfristig ist für mehrere Fahrzeugsegmente mit der Brennstoffzelle statt der Batteriezu rechnen.

Insgesamt ist deshalb die Förderung der Batteriezellenproduktion eher als politisch motivierte denn als ökonomisch sinnvolle Maßnahme zu bewerten. Wollen wir dies mit dem Geld der Steuerzahler unterstützen?

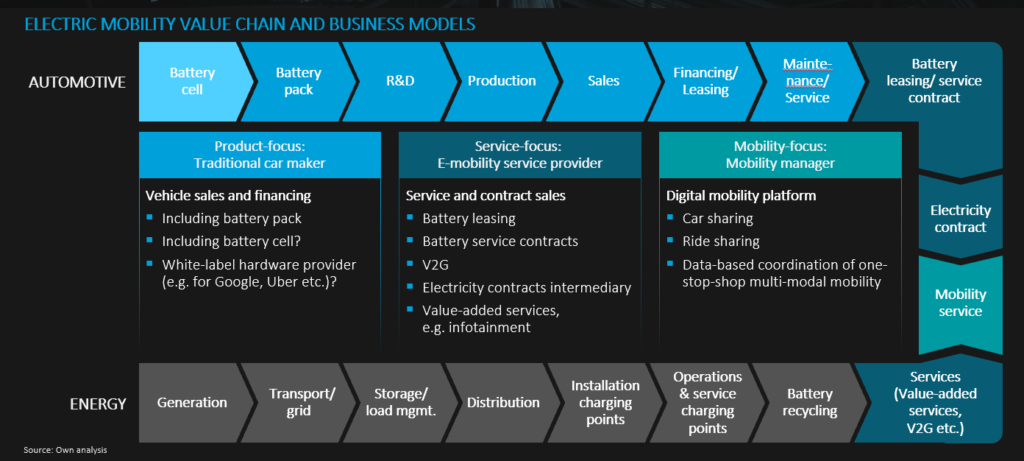

The automotive disruption and its impact on OEMs and suppliers

09 May 2019Do you remember the last time you took a picture with an analogue, non-digital camera? Chances are that this is quite some time ago. The younger generation doesn‘t even know what we are talking about…

The digital camera was a disruptive innovation to the photo industry. It has replaced the traditional, analogue camera. Formerly, established players such as Kodak or Leica have dominated the value chain. They have either disappeared or been restructured. Today, there are manufacturers such as Sony or Canon but it is us, the consumer, who records, develops, modifies and stores images based on their own taste.

The Automotive Disruption

The electric vehicle is a disruptive technology to the automotive industry. Such as the digital camera has dramatically changed the photo industry, the electric vehicle will dramatically change the automotive industry:

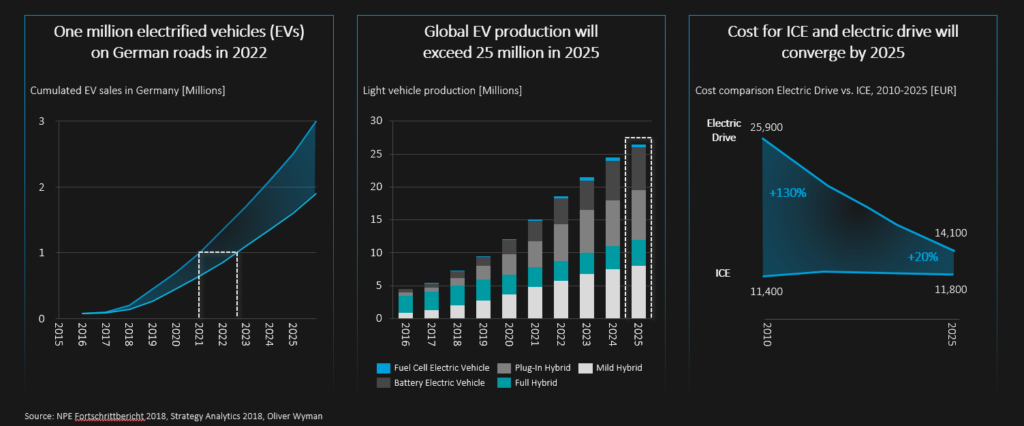

- We won‘t make the original goal of 2020, but in 2022 there will be one million electrified vehicles (EVs) on German roads

- We will produce more than 25 million EVs on a global level by 2025

- And in the same time horizon, we will see cost for internal combustion engine (ICE) and electric drive converge

The automotive disruption

What does that mean for manufacturers (OEMs) and suppliers?

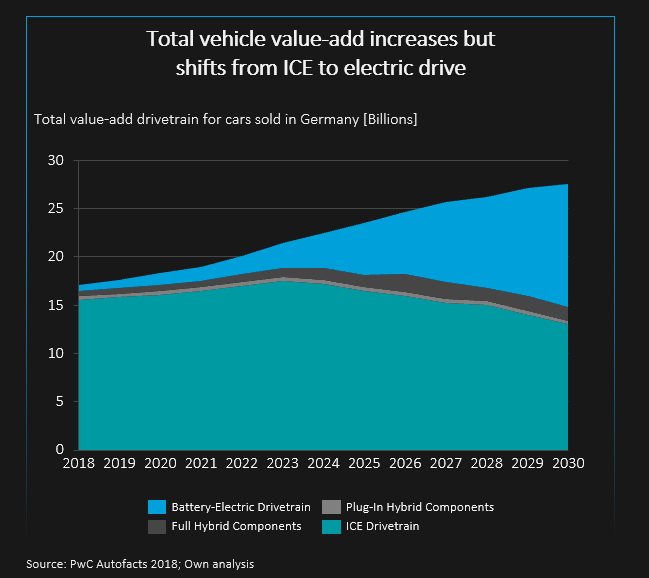

Until 2030 we will see a major shift in value-add from ICE to electric drive. This will result in major changes for OEMs: upstream on the supplier side and downstream at the customer interface.

Shift in value-add from ICE to electric drive

Upstream we will see the supplier base change significantly since numerous components will disappear and new components, especially the battery, will be added. Since the battery is such a key component, we expect OEMs to increase their vertical integration and insource huge parts of the battery value creation.

Downstream, we are already seeing a multitude of new players emerging that compete with and threaten OEMs at the customer interface: innovative manufacturers (e.g. Tesla), consumer electronics companies (e.g. Samsung, LG), utilities, tech giants (e.g. Google, Amazon) and mobility service providers (e.g. Uber). That‘s why we expect services such as battery service contracts, mobility and payment services to play a crucial role because they usually guarantee direct customer contact.

While this is rather an external market view, internally the new and additional components will massively increase complexity in the vehicle development process.

On the supplier side, this development will put significant pressure on current suppliers. We already mentioned that important components are eliminated, changed or added:

- eliminated: combustion engine, exhaust

- changed: gear box, transmission

- added: battery, electrics, power electronics

OEMs will try to reduce component cost by disaggregating certain modules and by insourcing components such as the battery pack. Moreover, most suppliers are forced to invest in existing technology (e.g. ICE improvement) and new technology at the same time.

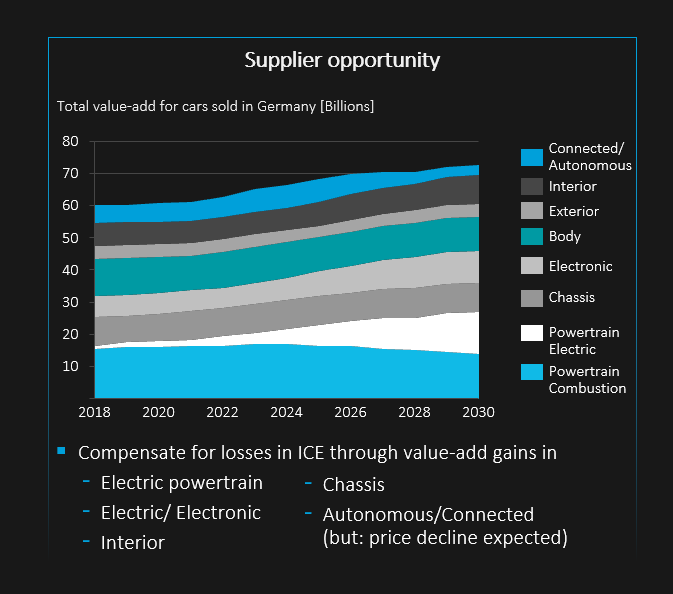

So is it a desperate situation? No, here comes the good news: total value creation for the car will increase, not decrease. Therefore suppliers can make up for losses in ICE in future key components such as electric powertrain, electric/ electronic, interior and connected/autonomous.

Total value creation by component cluster

OEM business models in a disrupted world